London’s Price Drop Map: Policy, Prime Boroughs, and the Canary in the Coal Mine

Today's discussion about the property market focuses more on what's truly influencing the figures, rather than just the number of properties on offer.

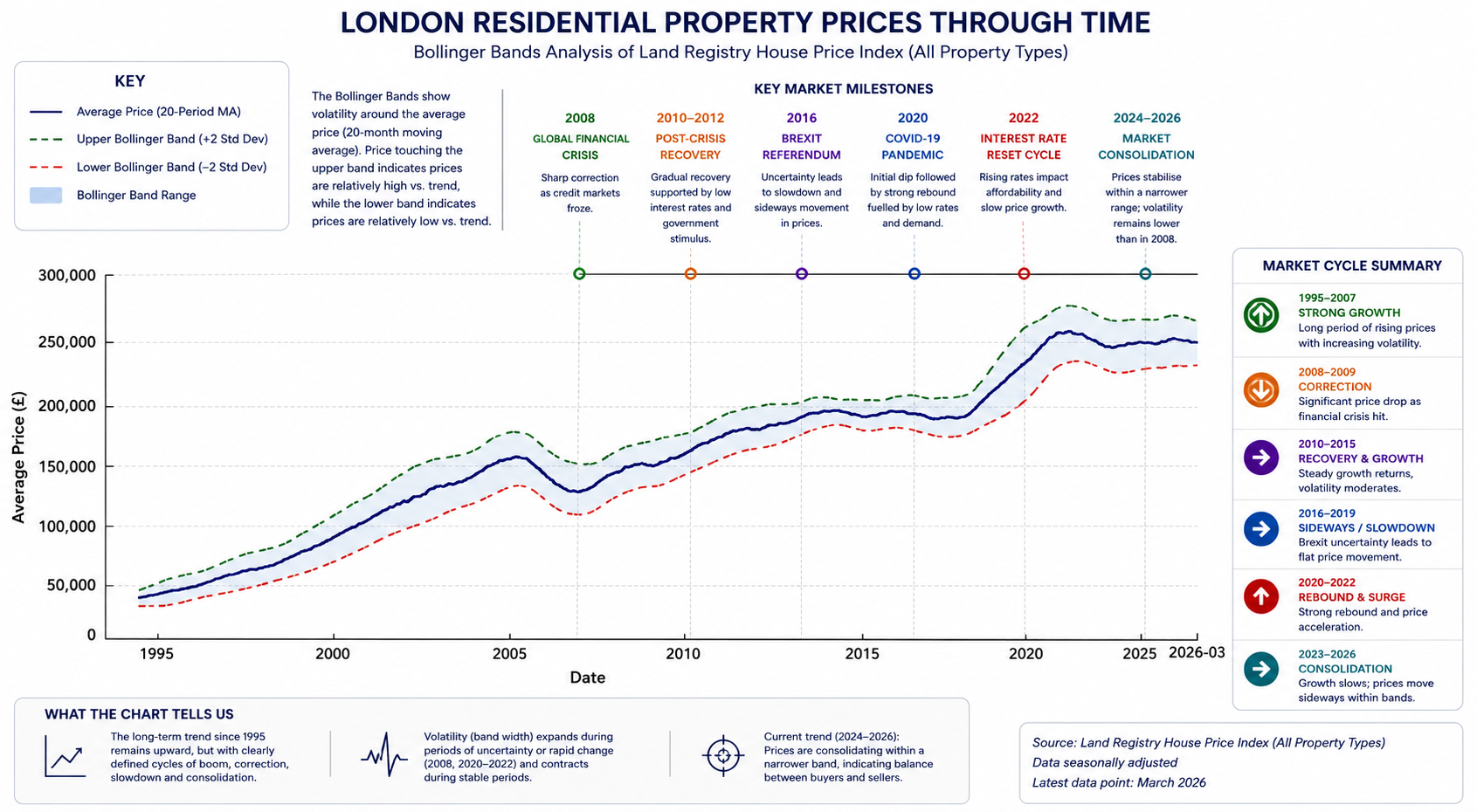

The latest UK House Price Index data for December 2025 reveals some intriguing trends in London. Several central boroughs are experiencing notable price declines compared to the previous year. For instance, prices in the City of Westminster dropped by approximately 14.8 per cent, Kensington and Chelsea by nearly 11.5 per cent, Camden by over 11 per cent, Tower Hamlets by just under 11 per cent, and Hammersmith and Fulham by close to 9.5 per cent.

Conversely, a few outer London boroughs are performing quite well. Bromley saw prices increase by over six per cent, Havering by more than five per cent, and Lewisham by nearly four per cent. Essentially, the London market isn’t moving in a straight line; it's fragmenting.

To truly understand why, we need to look beyond the raw figures. The boroughs experiencing the steepest price drops are also those traditionally supported by international investors, people capable of spending freely and those purchasing homes for personal use. When global confidence diminishes, these markets tend to react first because they rely less on local affordability and more on external factors.

Outer boroughs differ somewhat. Markets in places such as Bromley or Havering are primarily driven by local families, homeowners and long-term buyers, not by investors seeking quick profits. This kind of demand tends to be slower-moving and more stable. As a result, prices in these areas often remain more consistent, even amid economic uncertainty.

Mortgage rates remain a key factor. With inflation still somewhat unpredictable and the global situation unsettled, the Bank of England faces a tough balancing act. Rates may gradually decrease over time, but easing monetary policy won’t be straightforward. Financial markets are currently adopting a cautious approach rather than rushing to cut rates.

Adding to the uncertainty is the broader geopolitical landscape. The recent escalation of tensions with Iran in March 2026 unsettled global markets and energy prices. While such events don’t directly impact property values in London, they do influence inflation expectations, interest rate decisions, and investor confidence, all of which have a bearing on housing demand.

At the same time, affordability continues to be a major concern. In many parts of London, the link between income levels and property prices has been strained for years. When borrowing costs increase, even marginally, this imbalance quickly becomes evident. Some sellers are already adjusting their asking prices to attract buyers now more sensitive to mortgage costs.

Overall, the situation is one of increased uncertainty. While housing markets rarely collapse suddenly without warning, they can gradually lose momentum when several pressures converge. Factors such as interest rates, affordability challenges, global political tensions, and cautious lending practices all interact within this complex system.

Under such conditions, markets may enter what economists call a fragile equilibrium. Demand might still exist, and supply could remain limited, but confidence is weakening. When confidence falters, transaction volumes decline, negotiations widen, and price reductions become more common.

This does not automatically point to a crash, but it highlights how swiftly sentiment can shift when financial, political, and economic uncertainties align. Housing markets are interconnected with global influences, energy prices, currencies, and financial markets, all of which respond to the same pressures.

A stronger pro-growth economic policy could gradually shift this balance. Policies that encourage investment, improve business confidence and stabilise borrowing conditions would, over time, help restore momentum to the housing market. However, even the most carefully designed growth strategy cannot produce immediate results. Economic systems respond slowly, and policy effects typically unfold over years rather than months.

At present, the direction of travel appears different. Higher levels of public spending, expanding welfare commitments, tighter regulation and a progressively heavier taxation environment are increasingly shaping business behaviour and investor confidence. Measures such as high stamp duty rates, relatively low VAT thresholds affecting smaller businesses, and broader tax pressures on income and property transactions reduce the financial flexibility of both households and investors. When combined with relatively modest wage growth and limited household savings, these factors constrain purchasing power and reduce the pool of buyers able to enter or move within the market.

The London property market is particularly sensitive to these dynamics. Where confidence weakens and disposable capital becomes constrained, activity slows, and pricing pressure begins to emerge. While certain aspects of this environment may create opportunities for first-time buyers, especially where prices soften, this group simultaneously faces the most acute affordability challenge of all. Rising borrowing costs, high deposit requirements and limited disposable income mean that even modest improvements in pricing do not automatically translate into easier access to home ownership.

This brings us back to the central question behind the title of this article. Are the current developments in London’s housing market acting as a canary in the coal mine for the wider economy? Markets rarely move in isolation, and housing often reflects deeper economic conditions before they become visible elsewhere. When confidence weakens, transaction volumes fall, investors retreat, and sellers begin adjusting expectations.

Of course, this does not automatically mean that a market collapse is inevitable. However, it does suggest that the system is operating under pressure and that early warning signals are already visible. If such signals are recognised and addressed through balanced economic and growth-oriented policies, the market may stabilise and gradually regain confidence. If they are ignored, however, the accumulation of these pressures could eventually lead to far more serious consequences, including the possibility of a broader market correction or collapse.